Foreword

One of the major features of crypto is that they are decentralized, meaning they are not controlled by a single institution like a government or central bank, but instead are divided among a variety of computers, networks, and nodes. In many cases, cryptos make use of this decentralized status to attain levels of privacy and security that are typically unavailable to standard currencies and underlying transactions.

A group of developers came up with the idea for a DAO in 2016, but a lot of spirits, designs and utilizations of DAO have evolved with the fast changes in crypto markets. With recent major collapses and ongoing crypto winter, it is worth having a deeper look at where DAO is now and how it will act in the near future.

Similar to all major DEX, DuraFi should consider how to build the DAO infrastructure and user cases. As a consequence, the research depicts a general framework once our business vision becomes clearer.

Deep-Dive In DAO

DAO is a staple of web3. Web-native and blockchain-based. DAOs are intended to provide a new, democratized management structure for businesses, projects, and communities, in which any member can vote on organizational decisions just by buying/holding tokens of the project.

At a high level, DAOs works as blow:

-

DAO founders create a new cryptocurrency, known as a governance token;

-

They distribute these tokens to users, backers, and other stakeholders;

-

Each token corresponds to a set amount of voting power within the organization. Each token also corresponds to a price on the secondary market, where it can be bought and sold at will. While this process is often described as a way to decentralize power, governance token data suggests that DAO ownership is actually highly concentrated.

The concentration of governance token holdings

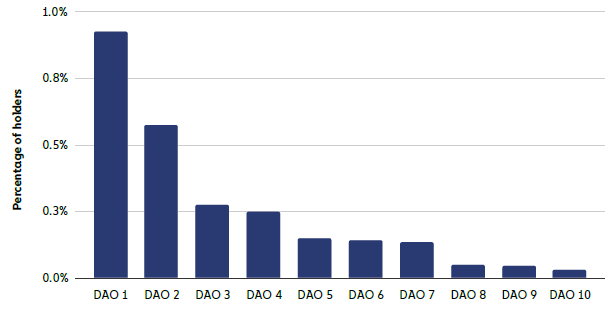

By analyzing the distribution of ten major DAOs’ governance tokens, it is a surprise to know that across several major DAOs, less than 1% of all holders have 90% of voting power.

==Share of users holding 90% of all governance tokens by DAO==

The fact has meaningful implications for DAO governance. Saying, if just a small portion of the top 1% of holders worked together, they could theoretically outvote the remaining 99% on any decision. This has obvious practical implications and, in terms of investor sentiment, likely affects whether small holders feel that they can meaningfully contribute/gain to/from the proposal process.

The impact of high concentration on DAO governance

For a governance token holder, there are 3 key governance actions.

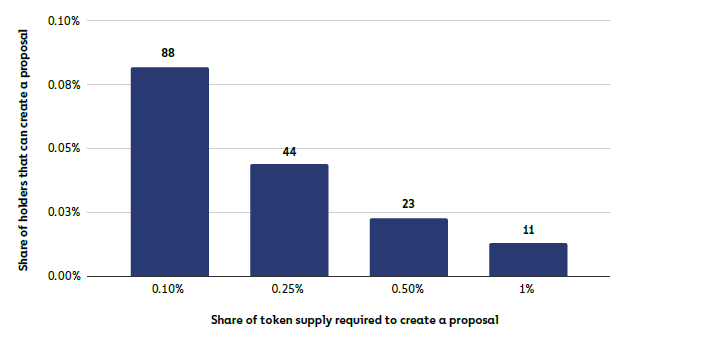

Per these ten DAOs proposal requirements, it could conclude as below:

-

A user must hold between 0.1% and 1% of the outstanding token supply to create a proposal.

-

A user must hold between 1% and 4% to pass it. Using these ranges as lower and upper bounds, we find that between 1 in 1,000 and 1 in 10,000 of these ten DAOs’ holders have enough tokens to create a proposal.

==Share and number of holders that can create a proposal==

There are several tradeoffs at play here. If too many holders can create a proposal, the average proposal’s quality may fall, and the DAO may be riddled with governance spam. But if too few can, the community may come to feel that “decentralized governance” rings false.

When it comes to single-handedly passing a proposal, between 1 in 10,000 and 1 in 30,000 holders have enough tokens to do so. Overly concentrated voting power in DAOs can result in decision-making that seemingly contradicts the tenets of decentralization on which web3 is built.

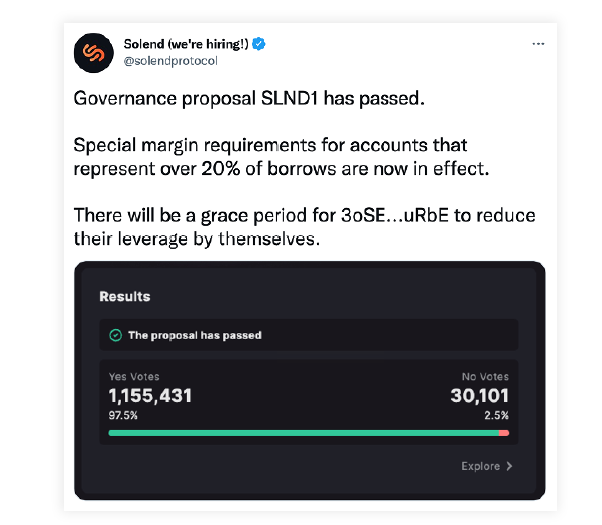

For instance, in June 2022, the DAO governing the Solana-based lending protocol Solend faced a problem: Solana’s price was dropping, and if it fell much further, the protocol’s biggest whale user would face a margin call that could render Solend insolvent and send roughly $20 million worth of Solana onto the market, potentially tanking the asset’s price and upending the entire Solana ecosystem. The DAO called a vote to take control of the whale’s account and liquidate its position through OTC desks, rather than the open market.

The proposal passed easily, with over 1.1 million “yes” votes to 30,000 “no” votes. However, more than 1 million of those votes came from a single user with enormous governance token holdings. Without their vote, the motion wouldn’t have passed the 1% participation rate necessary for quorum.

The decision triggered a backlash from the cryptocurrency community, with many questioning how a platform could claim to be decentralized and then take control of a user’s funds against their will. Following this, the Solend DAO voted again to invalidate the proposal, and the whale user eventually began to unwind their position. While the crisis was averted in this case, it raises questions about the ability of a DAO to act in the best interest of all participants when some voters control such an outsized share of governance tokens.

How do DAOs govern?

Actual governance processes vary enough from DAO to DAO.

Example: Uniswap Governance

Uniswap is a DEX, and, like many DeFi protocols, it is governed by a DAO. Anyone who holds Uniswap’s UNI is a member of this DAO. They can participate in governance by delegating their voting rights to their own or another’s address, by publicizing their opinions, or by submitting their own proposal. The contents of these proposals vary widely.

However, before someone can submit a proper proposal, their idea must pass the first two phases: temperature checks and consensus checks.

-

The temperature check determines whether there is sufficient community will to change the status quo. At the end of the two days, a majority vote with a 25,000 UNI yes-vote threshold wins.

-

The consensus check establishes formal discussion around a potential proposal. At the end of five days, a majority vote with a 50,000 UNI yes-vote threshold wins.

If both checks pass, an official governance proposal can be put to a vote. Then, there’s a seven-day deliberation period to discuss the merits of this proposal on governance forums. If at the end of this period there are at least 40 million yes-votes with no-votes as a minority, the proposal has passed, and will be enacted after a two-day timelock.

Example: Dream DAO Governance

Not all DAOs function like Uniswap, but most at least run on similar infrastructure, using voting systems like Snapshot and chat servers like Discord. Dream DAO is no exception, though its mission and therefore its governance process is necessarily unique.

Dream DAO is an impact-oriented DAO created by 501(c)(3) charity Civics Unplugged and designed to provide diverse Gen Zers globally with the training, funding, and community they need to use web3 to improve humanity. Their governance process is run by holders of SkywalkerZ — NFTs.

The governance tokens and fundraising incentives for anyone interested in donating to the program. For every SkywalkerZ NFT purchased by a donor, a new SkywalkerZ is reserved for a future Gen Zer to join as a voting member, thereby receiving power in the DAO without needing to pay. The purchaser of the NFT can apply to join the DAO and become a voting member as well, or they can leave it to the Gen Z student they’ve sponsored — either way, the NFT is theirs to keep.

By removing financial barriers from the process of participating in DAO governance, Dream DAO empowers its target audience – future Gen Z leaders – to influence decision-making, immerse themselves in web3, and leverage blockchain technologies positively.

Where are DAOs most common and well-funded?

DAOs span the entire length of web3. They govern:

-

DeFi protocols like Uniswap ($UNI) and Sushi ($SUSHI).

-

Social clubs like Friends With Benefits ($FWB) and Bored Ape Yacht Club ($APE).

-

Grant-makers like Gitcoin ($GTC) and Seed Club ($CLUB).

-

Play-to-earn gaming guilds like Good Games Guild ($GGG) and Yield Guild Games ($YGG).

-

NFT generators like Nouns (1 NFT = 1 vote).

-

Venture funds like MetaCartel and Orange DAO.

-

Charities like Big Green DAO and DreamDAO (1 SkywalkerZ = 1 vote).

-

Virtual worlds like Decentraland ($MANA) and Sandbox ($SAND).

-

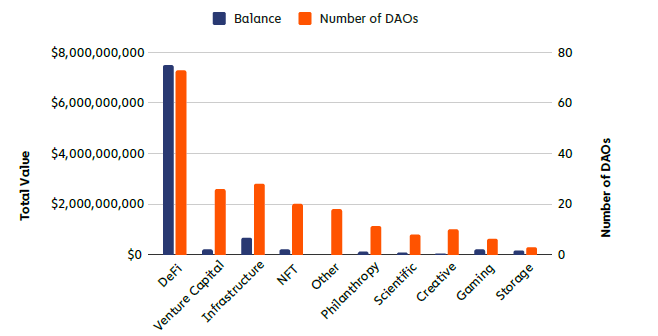

Else In terms of the number of DAOs and their treasury sizes, however, DeFi-related DAOs have a giant lead. The DeFi category accounts for 83% of all DAO treasury value held and 33% of all of the DAOs by count.

==Total assets held and number of DAOs by web3 category==

There are also a large number of DAOs focused on venture capital, infrastructure, and NFTs, suggesting that DAOs are appealing to investors, developers, and artists. Their on-chain treasuries, however, are relatively tiny.

To be fair, the lines between these categories are blurry. Gaming DAOs often engage with NFTs, venture DAOs often provide funding to DeFi, and infrastructure DAOs support all of the above categories.

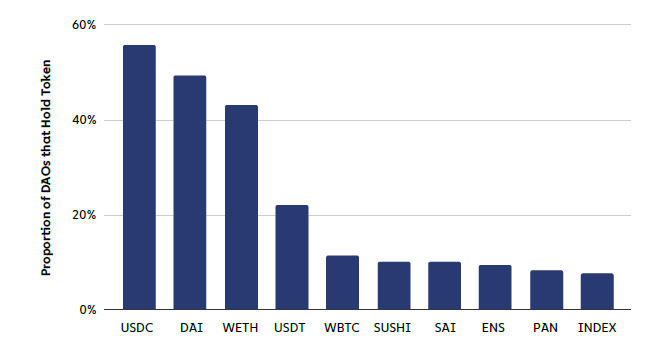

Treasury management

Even though DAOs vary in type and size, most of their on-chain treasuries hold similar cryptocurrencies. The most commonly held cryptocurrency is USDC, with over half of the 197 DAOs we analyzed holding a balance of USDC.

==Cryptocurrencies held by the most DAOs==

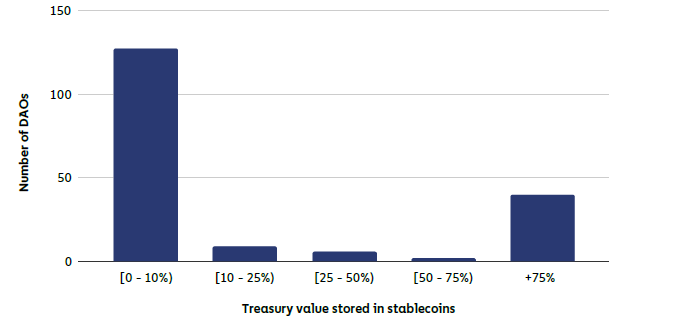

However, stablecoins seldom account for a majority of an on-chain treasury’s value. On average, 85% of DAOs’ on-chain treasuries are stored in a single asset, and that asset is a stablecoin in only 23% of the DAOs.

==Percentage of DAO treasury allocated to stablecoins==

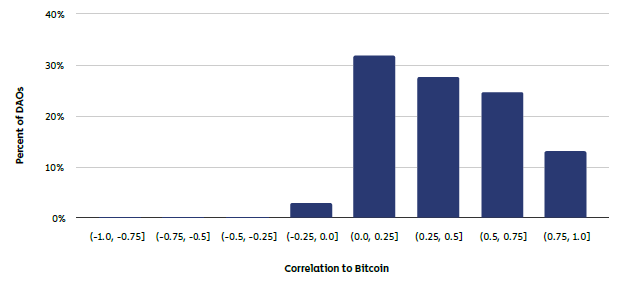

These on-chain treasuries are roughly as volatile as Bitcoin. By assuming DAOs’ current holdings are their historical portfolios over the last year, we find that:

-

The average DAO with assets over $1 million has an annualized volatility of 82%, versus 69% for Bitcoin.

-

The average DAO with assets over $1 million suffered a maximum drawdown of 51% over the past year, compared to Bitcoin’s drawdown of 72%.

DAO treasury values are also fairly correlated with Bitcoin price movements. 38% of on-chain DAO treasuries have correlations with Bitcoin that are between 0.5 and 1.00.

==How strongly DAO treasury values correlate with Bitcoin price movements==

One of the most interesting areas of DAO treasury management that has yet to take off is in M&A. M&A makes sense for DAOs because it allows them to get into adjacent areas without having to develop internal tooling. As the DAO model matures, it is unlikely that M&A will become more commonplace.

DAOs thus far have also been fairly limited in terms of the types of instruments they use and hold. For example, few DAOs to date have used loans or credit, perhaps due to their uncertain legal status. As DAOs mature, we are likely to see more standardized regulations, management strategies, and reporting practices.

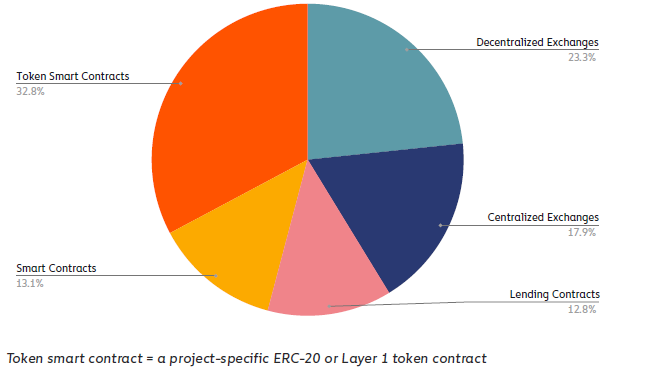

DAOs Contributor composition

==Where DAO contributions come from==

DAO participants are advanced users of cryptocurrency services. Only 17.9% of DAO treasury funds came from centralized services, while the remaining 82.1% originated at decentralized services. This suggests that most DAO contributors also engage with DeFi platforms and likely self-host their cryptocurrency.

The future of DAOs

As DAOs gain momentum, Superdao streamlines DAO creation; Snapshot simplifies governance; and Coin Center advocates for the industry on Capitol Hill…etc.

As they continue to expand, it will be interesting to see what they can accomplish, what they will become, and to what extent they will achieve their goal to decentralize the ownership of the internet. With the proliferation of DAOs today, we’ll have plenty of chances to see.